泰格医药(300347)

3Q22 earnings in line. Tigermed reported 3Q22 revenue of RMB1,812mn, up 35% YoY, attributable net income of RMB413mn, down 22% YoY, and attributable recurring net income of RMB421mn, up 29% YoY. Excluding COVID-19 revenue, we estimate 3Q22 revenue increased by c.42% YoY. The declining attributable net income in 3Q22 was mainly attributable to the fair value losses of RMB11mn, compared with fair value gains of RMB211mn in 3Q21. Gross profit margin (GPM) continuously improved to 40.9% in 3Q22 from 38.8% in 1Q22 and 40.6% in 2Q22, thanks to the shrinking size of the low-margin COVID-19 related revenue (due to pass-through revenue to sub-contractors in overseas markets) as well as the growth of US$-denominated services, such as data management and statistical analysis (DMSA) and laboratory services provided by Frontage, which benefited from US$ appreciation in 3Q22. Non-COVID-19 related new orders increased by c.35%/30% YoY in 9M22/3Q22, respectively, indicating sustainable growth of core business.

Consistently focus on high-margin business. Management has prioritized the expansion of high-margin businesses, including clinical trials operation,DMSA and some emerging services while takes a relatively conservative strategy on the SMO business given its low profitability nature. According to management, the Company has further increased its market share in China clinical CRO market for innovative drugs to c.20% in 3Q22, which represented the Company’s strong competency and high customer recognition. DMSA successfully sealed a strategic cooperation deal with a global Top10 pharma in the past quarter. Additionally, Tigermed has adopted a proactive hiring strategy and allocated more human resources to high margin business in 3Q22. We think the strategic change is critical and necessary for Tigermed to further enhance its leading position for its core business given the intensifying competition in China market in recent years.

Globalization on track. Tigermed has built local BD teams to explore business opportunities in Europe and the US. The Company has participated in large-scale Phase III multi-regional clinical trials (MRCT) in multiple middle and western European countries. The Company also took full advantages of its experiences in COVID-19 vaccine projects of Chinese clients to expand business opportunities in developing countries, including Indonesia, Brazil, Chile and Pakistan. These developing countries could be potential markets for Chinese drug makers, which will create additional demand for Tigermed’s clinical CRO services.

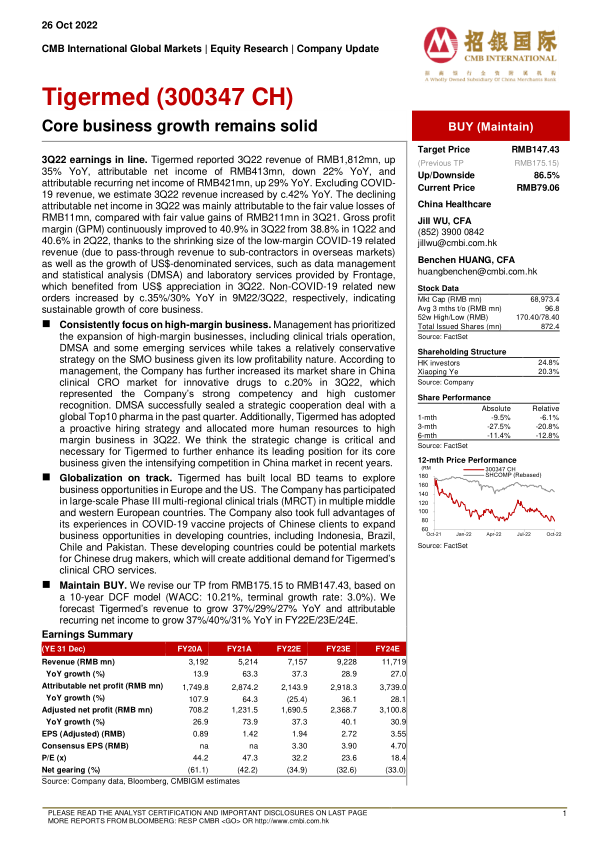

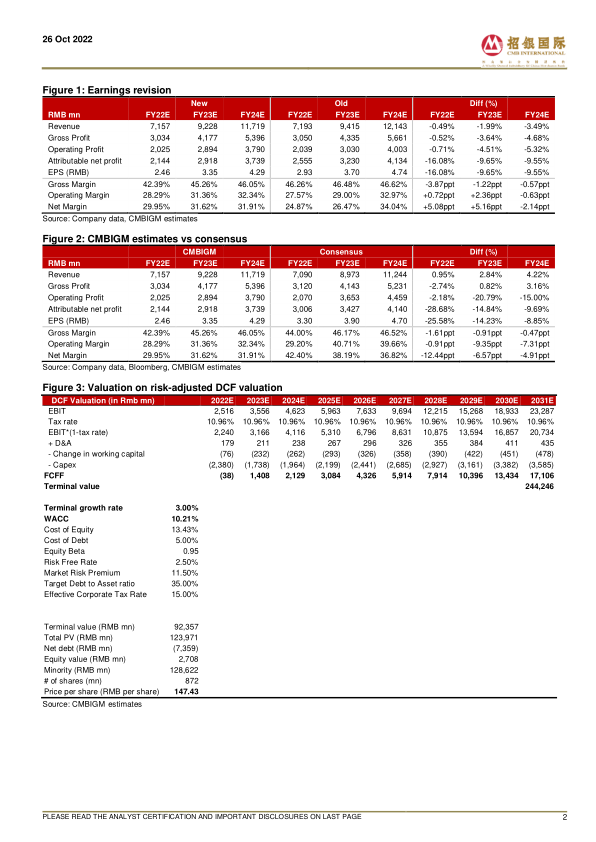

Maintain BUY. We revise our TP from RMB175.15 to RMB147.43, based on a 10-year DCF model (WACC: 10.21%, terminal growth rate: 3.0%). We forecast Tigermed’s revenue to grow 37%/29%/27% YoY and attributablerecurring net income to grow 37%/40%/31% YoY in FY22E/23E/24E.

微信扫一扫-立即使用

微信扫一扫-立即使用