迈瑞医疗(300760)

Mindray reported9M24revenue of RMB29.5bn,up by8.0%YoY.Attributable netprofit increased by8.2%YoY to RMB10.6bn.Revenue in3Q24grew by1.4%YoY to RMB9.0bn while attributable net profit decreased by9.3%YoY toRMB3.1bn.The slowdown in revenue growth can primarily be attributed tolackluster procurement activities in domestic public hospitals and weakeneddemand for IVD testing,particularly in lower-tier hospitals.Consequently,Mindray's domestic revenue fell by9.7%YoY in3Q24.Additionally,GPM in3Q24decreased by4.8pcts QoQ due to updates in accounting guidelines.

Domestic market remained under pressure,although signs of recoveryin procurement are emerging.1)IVD:Domestic revenue grew by17%YoYin9M24.Nationwide DRG implementation had a negative impact on thediagnosis demand in lower-tier hospitals which were the main contributors toMindray's domestic IVD revenue.To counter act this,Mindray activelyexpanded its IVD business into top hospitals through its TLA and IT solutions.We expect Mindray to install over150TLAs in2024E.2)MIS:Domesticrevenue grew by over10%YoY in9M24driven by the strong volume ramp-up of ultra-high-end Resona A20ultrasound system.3)PMLS:Domesticrevenue decreased by28%YoY in9M24.The decline was influenced by

environment.However,with accelerated issuance of special bonds,andstronger government support to address local debt issues,we expectdomestic equipment demand to recover in2025E.

Healthy growth in overseas business.In3Q24,Mindray’s overseasrevenue increased by18.6%YoY with strong performances in Europe(+29%YoY),APAC(+32%YoY)and LatAm(+25%YoY),although there was someweakness in the US market.Driven by breakthroughs in medium-to-largevolume labs,Mindray’s overseas IVD revenue increased by32%YoY in9M24,accounting for28%of total overseas revenue.Mindray hasaccelerated its overseas localization efforts.As of3Q24,Mindray launchedlocal manufacturing in9countries,8of which are related to IVD.Additionally,emerging businesses such as minimally invasive surgery(+50+%YoY),AED(+50+%YoY)and animal medical(+30+%YoY)grew significantly in9M24.These emerging businesses contributed over10%to Mindray’s overseasrevenue.We expect IVD and emerging businesses to become the primarygrowth drivers for Mindray’s overseas businesses.

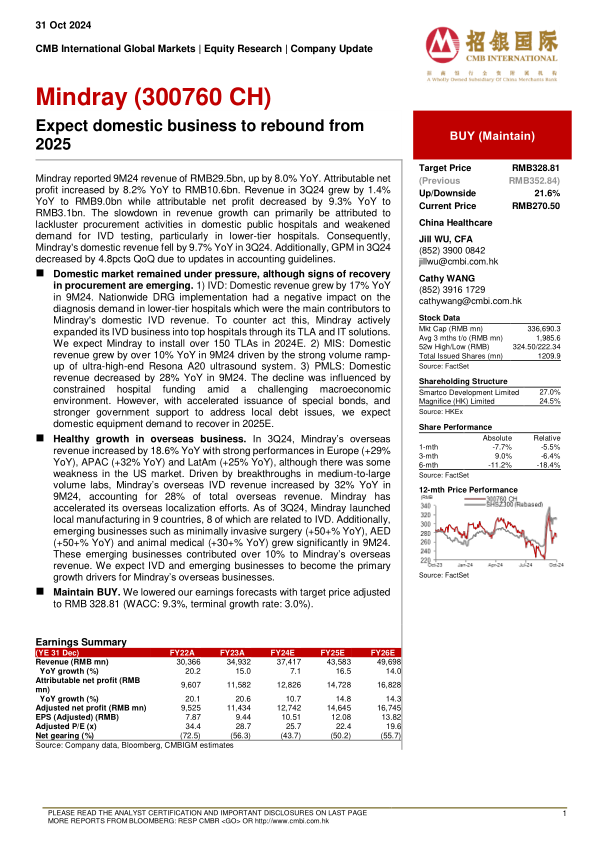

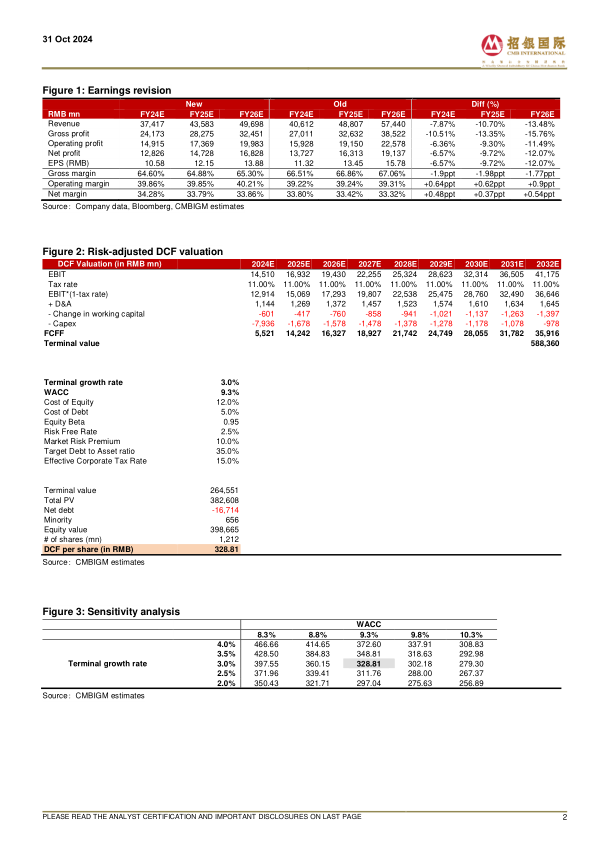

Maintain BUY.We lowered our earnings forecasts with target price adjustedto RMB328.81(WACC:9.3%,terminal growth rate:3.0%).

微信扫一扫-立即使用

微信扫一扫-立即使用