药明康德(603259)

WuXi AppTec reported better-than-expected 1H25 results, with revenueincreasing by 20.6% YoY (including 24.2% YoY growth for continuing operations)and adj. non-IFRS net profit surging by 44.4% YoY. Revenue from continuingoperations and adj. non-IFRS net profit accounted for 47.5% and 54.4%,respectively, of our full-year forecasts, both higher than the historical ranges.WuXi AppTec delivered strong operational execution, despite ongoing macrouncertainties. As such, mgmt. raised its full-year guidance for 2025, expectingrevenue of continuing operations to grow by 13-17% (vs prior guidance of 10-15%) and adj. non-IFRS net profit margin to expand in 2025.

Robust commercial demand drives CDMO outperformance. The robustdemand for late-stage clinical and commercial manufacturing has been a keygrowth driver for the global CXO industry in the post-COVID era. As a globalleader in the chemical drug CDMO sector, WuXi AppTec has substantiallybenefited from this trend. In 1H25, its TIDES revenue surged by 141.6% YoYthanks to faster-than-expected manufacturing capacity ramp-up. Mgmt raisedits full-year guidance for TIDEs revenue growth from 60% to 80%. Revenuefrom small molecule D&M grew by 17.5% YoY, marking a notable reboundfrom the negative growth seen in 2023/2024. In addition, the volatilities in USChina tariffs seemed to have limited impact to the Company’s first halfoperation, in our view. Despite ongoing volatility in the global macroenvironment, we believe that the sustained demand for commercial drugmanufacturing is likely to continue, supporting the growth of leading CDMOplayers like WuXi AppTec.

Expanding global capacity to support long-term growth. As of end-1H25,WuXi AppTec’s backlog impressively grew by 37.2% YoY, with backlog ofTIDES increasing even more strongly at 48.8% YoY. The mgmt. reiteratedtheir plan to increase the Company’s peptide capacity to over 100k liters bythe end of 2025 to support the demand from both existing commercialprojects and growing pipelines. At the same time, capacity expansion effortsare underway at multiple sites, including Changzhou (China), Singapore, theUS and Switzerland. WuXi AppTec has reaffirmed its capex target of RMB7–8bn in 2025, and anticipated possible increases in capex in the coming years.

Recovery in early-stage R&D still takes time. While revenue from earlystage R&D services showed sequential improvements in 1H25 over 2024,mgmt. viewed that a meaningful recovery in early-stage R&D demand willtake time. Early-stage R&D services contribute ~30% of the Company’s totalrevenue. The global biotech financing usually serves as an early indicator ofearly-stage R&D demand.

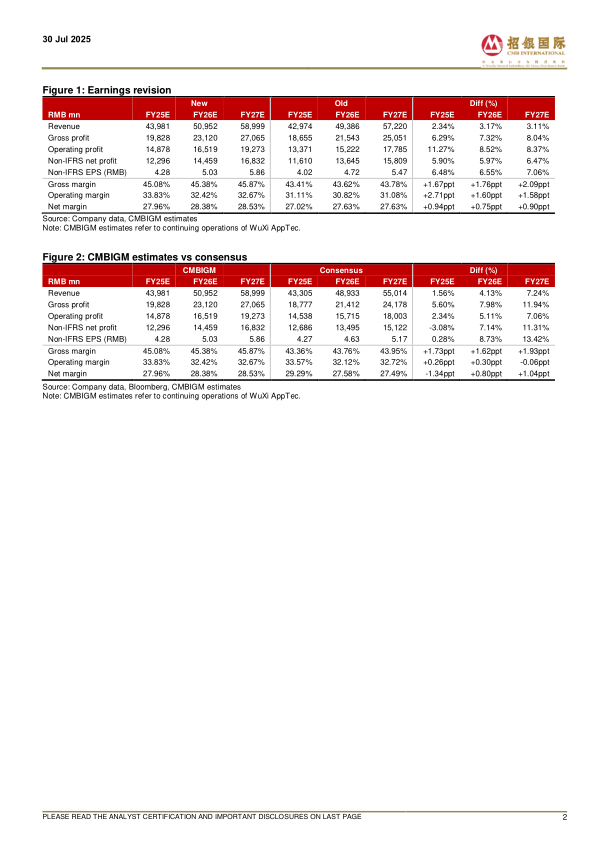

Maintain BUY. We raise our DCF-based TP from RMB77.22 to RMB116.56(WACC: 9.42%, terminal growth: 2.00%; both unchanged), to factor in theupgraded guidance and the improved macro environment such as the USChina tariff. We now expect revenue from continuing operations to grow by16.0%/ 15.9%/ 15.8% YoY and adjusted non-IFRS net profit to grow by16.2%/ 17.6%/ 16.4% YoY in 2025E/ 26E/ 27E, respectively

微信扫一扫-立即使用

微信扫一扫-立即使用