泰格医药(300347)

Tigermedreported1Q23revenueofRMB1,805mn,down0.7%YoY,andattributablerecurringnetincomeofRMB381mn,up0.7%YoY.1Q23revenue/attributablerecurringnetincomeaccountedfor21.2%/19.2%respectivelyofour2023full-yearestimates,whichwereinlinewithitshistoricalaveragelevel.1Q23revenuewouldgrowby27-28%YoYifexcludingCOVIDrelatedrevenue.Grossprofitmargin(GPM)in1Q23was39.7%,improvingby1.6pptQoQand0.8pptYoY,thankstothedecreasedproportionofrevenuefromCOVID-19relatedprojects(includingpass-throughrevenuetooverseassub-contractors)aswellasbusinessnormalizationinChinasinceFeb2023.Accordingtomanagement,GPMwouldbeabove41%ifexcludingCOVIDpass-throughrevenue.Neworderssignedin1Q23waslargelyflatYoY,whilemanagementexpectsasignificantpickupinnewordersgrowthfrom2Q23giventherecoveryofrequestsforproposalsince1Q23.

Operation fully resumed after the COVID pandemic, laying a soundfoundation for full-year growth. Management indicated that COVIDinfection among employees had disrupted business operations in Jan 2023,with China-based laboratory services taking the most hit. According toFrontage (1521 HK), revenue declined by 1.8% YoY while adjusted net profitdropped by 77% YoY in 1Q23. With business operation resumed normal,management expected both revenue and GPM to see sequentialimprovements in 2Q23.

Globalization remains a business focus. Tigermed acquired a Croatiabased clinical CRO, Marti Farm, in Jan 2023, further enhancing its servicecapability in Europe. The Company is integrating its BD team in Europe toenhance BD capabilities. In the US, Tigmerd aims to double its local clinicaloperation team to over 100 staff in 2023. The Company’s strategies inEurope and US include collaborating with small- to mid- sized clients withrelatively inadequate access to resource of global clinical CROs andChinese clients going to developed markets. Additionally, Tigermed takes aproactive approach in Southeast Asia and Latin America. Such regions arepotential end markets for Chinese drug developers, which will createadditional demand for Tigermed in overseas market.

Operating cash flow to recover. Net operating cash flow substantiallydeclined by 91% YoY to RMB29mn, due to 1) delay in part of cost paymentfrom 4Q22 to 1Q23 due to COVID outbreak; 2) sizable income from COVIDvaccine projects in 1Q22 which caused a high base; and 3) the increasingstaff cost due to the growing employee number. Management guided netoperating cash flow to rebound from 2Q23.

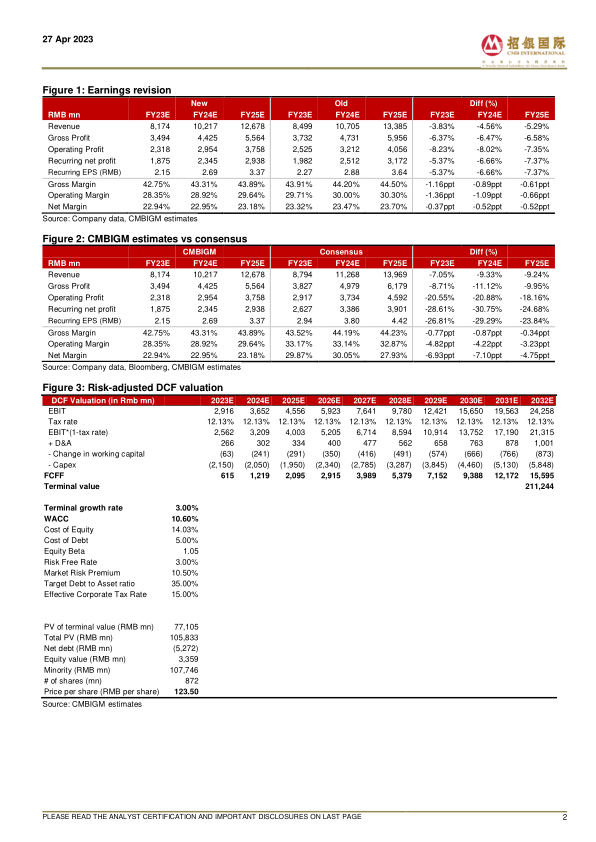

Maintain BUY. We revised our TP from RMB134.24 to RMB123.50, basedon a 10-year DCF model (WACC: 10.6%, terminal growth: 3.0%), to factorin slower revenue growth projection. We forecast Tigermed’s revenue togrow 15.4%/ 25.0%/ 24.1% YoY and attributable recurring net income to grow21.8%/ 25.0%/ 25.3% YoY in FY23E/ 24E/ 25E, respectively.

微信扫一扫-立即使用

微信扫一扫-立即使用